Brought to you by:

Enterprise Strategy Group | Getting to the Bigger Truth™

ESG WHITE PAPER

DIGITAL TRANSFORMATION:

The CIO Imperative

DIGITAL TRANSFORMATION:

The CIO Imperative

The Multicloud Opportunity for Partners with Dell APEX

The Multicloud Opportunity for Partners with Dell APEX

By Kevin Rhone, Practice Director; and Scott Sinclair, Senior Analyst

AUGUST 2022

Introduction

Figure 1. IT Complexity Continues to Be Driven by Multiple Factors

What do you believe are the biggest reasons your organization’s IT environment has become more complex? (Percent of respondents, N=329, five responses accepted)

Source: ESG, a division of TechTarget, Inc.

Overview and Opportunity

New Consumption Patterns Translate into Partner Opportunity

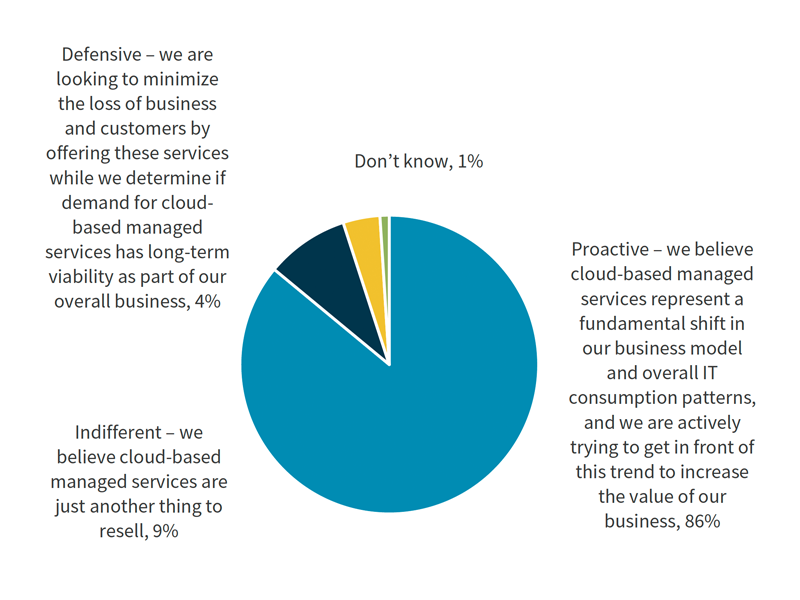

Figure 2. IT Partners Are Aggressively Adopting As-a-service Business Models

Which statement best describes your organization’s current organizational philosophy toward cloud-based managed services? (Percent of respondents, N=346)

Source: ESG, a division of TechTarget, Inc.

With Opportunity Comes Some Challenges

Customers Making the Move See Real Benefits

Figure 3. Companies Increasingly Prefer Pay-as-you-go Payment Models

Assuming the net-cost was the same, which of the following do you believe would be your organization’s preferred payment model for on-premises data center infrastructure? (Percent of respondents)

Source: ESG, a division of TechTarget, Inc.

What’s In It for Customer IT Teams?

Figure 4. IT Partners Are Aggressively Adopting As-a-service Business Models

Source: ESG, a division of TechTarget, Inc.

How Do Progressive IT Organizations Move Up the Maturity Curve? (Hint: With Help from Dell Technologies, Intel, and their IT partners)

Theme #1 – The CIO Imperative of as-a-Service Transformation

Figure 5. Most Important Digital Transformation Objectives

What are your organization’s most important objectives for its digital transformation initiatives? (Percent of respondents, N=694, three responses accepted)

Source: ESG, a division of TechTarget, Inc.

Figure 6. Transitioning to aaS is Fundamental

Agree or Disagree: Delivering dedicated infrastructure “as-a-Service” is critical to our IT operations to keep up with user demands. (Percent of respondents, N=1,000)

Source: ESG, a division of TechTarget, Inc.

Figure 7. Organizations’ Digital Transformation Initiatives

Which of the following best describes your organization’s digital transformation initiatives? (Percent of respondents, N=372)

In which of the following areas does your organization have an active digital transformation project? (Percent of respondents, N=270, multiple responses accepted)

Source: ESG, a division of TechTarget, Inc.

Figure 8. Data Center Strategy Is Becoming More Cloud-like

Which of the following is or likely will be part of your organization’s strategy for on-premises data center environments over next three years? (Percent of respondents, N=372, multiple responses accepted)

Source: ESG, a division of TechTarget, Inc.

Why Do Customers Rely on Dell Technologies’ Partners?

Theme #2 – Navigating Multicloud Complexity

Why Do Customers Rely on Dell Technologies’ Partners?

Figure 9. Cloud Selection Criteria

What are your organization’s biggest drivers for choosing a public cloud service for production workloads? (Percent of respondents, N=363, multiple responses accepted)

Source: ESG, a division of TechTarget, Inc.

Figure 10. Challenges When Leveraging Multiple CSPs

What are the greatest challenges your organization faces as a result of using multiple CSPs? (Percent of respondents, N=279, multiple responses accepted)

Source: ESG, a division of TechTarget, Inc.

Theme #3 – Innovating with Data

Figure 11. Growth in Data Centers Predicted

How many data centers did your organization operate 5 years go? How many data centers does your organization operate today? How many data centers do you expect your organization will have in five years? (Percent of respondents, N=372)

Source: ESG, a division of TechTarget, Inc.

Figure 12. The Importance of Infrastructure Modernization

How much of an investment priority is your organization’s application infrastructure modernization strategy relative to other aspects of IT over the next 18-24 months? (Percent of respondents, N=372)

Source: ESG, a division of TechTarget, Inc.

Why Do Customers Rely on Dell Technologies Partners?

Figure 13. Preferences for On-premises Application Infrastructure

What is your organization’s preference for an on-premises application infrastructure? (Percent of respondents, N=372)

Source: ESG, a division of TechTarget, Inc.

Theme #4 – Meeting the Needs of End-users and IT Alike in The ‘Work From Anywhere’ World

Figure 14. Top Five Benefits Organizations Realized from VDI/DaaS

Which of the following benefits has the IT organization realized as a result of its use of VDI/ DaaS? (Percent of respondents, N=338, multiple responses accepted)

Source: ESG, a division of TechTarget, Inc.

Figure 15. Top Five Factors for Investment in EUC Technology Solutions

What are the most important factors for your organization when considering investments in EUC technology solutions? (Percent of respondents, N=378, three responses accepted)

Source: ESG, a division of TechTarget, Inc.

Why Do Customers Rely on Dell Technologies Partners?

The Bigger Truth

• Allows partners to respond to changing customer consumption models and support long-term customer value.

• Supports partner business model transformation in their organizations.

• Syncs partner programs, support, and rewards for their evolving GTM strategies:

o Consistent partner program benefits regardless of selling motion.

o Consistent rewards for both CapEx and OpEx purchase, supporting customer purchase options.

• Creates a pathway to partner profitability—a “bridge” to sustainable partner value through:

o Customer engagement at a strategic level (IT + LOB).

o Renewal and expansion business, supported by high-value ongoing services.

This ESG White Paper was commissioned by Dell Technologies and is distributed under license from TechTarget, Inc.

© Intel Corporation. Intel, the Intel logo, and other Intel marks are trademarks of Intel Corporation or its subsidiaries. Other names and brands may be claimed as the property of others.

All product names, logos, brands, and trademarks are the property of their respective owners. Information contained in this publication has been obtained by sources TechTarget, Inc. considers to be reliable but is not warranted by TechTarget, Inc. This publication may contain opinions of TechTarget, Inc., which are subject to change. This publication may include forecasts, projections, and other predictive statements that represent TechTarget, Inc.’s assumptions and expectations in light of currently available information. These forecasts are based on industry trends and involve variables and uncertainties. Consequently, TechTarget, Inc. makes no warranty as to the accuracy of specific forecasts, projections or predictive statements contained herein.

This publication is copyrighted by TechTarget, Inc. Any reproduction or redistribution of this publication, in whole or in part, whether in hard-copy format, electronically, or otherwise to persons not authorized to receive it, without the express consent of TechTarget, Inc., is in violation of U.S. copyright law and will be subject to an action for civil damages and, if applicable, criminal prosecution. Should you have any questions, please contact Client Relations at cr@esg-global.com.

Enterprise Strategy Group | Getting to the Bigger Truth™

Enterprise Strategy Group is an IT analyst, research, validation, and strategy firm that provides market intelligence and actionable insight to the global IT community.